Heavy equipment is not just an investment for construction businesses—it’s the foundation of your operations. These machines, from excavators to bulldozers, are critical to getting the job done. However, with such high-value equipment, the potential for loss or damage poses a significant risk. Heavy equipment insurance is designed to protect your construction business, but understanding how much it costs requires examining a range of factors.

This guide provides an overview of the insurance options available, the risks they cover, and key considerations for managing costs effectively. By understanding your coverage options and what impacts premiums, you can make informed decisions to safeguard your equipment and keep projects moving forward.

What is Heavy Equipment Insurance?

Heavy equipment insurance can be customized to protect construction businesses from the financial risks of owning and operating large machinery. This type of insurance typically covers physical damage, theft, and liability losses. Whether you own excavators, bulldozers, cranes, or other machinery, having a comprehensive policy ensures that your business can recover quickly from unexpected setbacks.

Heavy equipment insurance can include specific endorsements like inland marine coverage. You can tailor options to safeguard your machinery on-site, in transit, or at storage locations, making it a critical investment for contractors and construction businesses. By securing the right coverage, you can minimize downtime and financial loss, keeping your projects on track.

Keep reading to learn more about the policies you need, with expert advice from Rachel Pinsonneault, commercial lines underwriter at Central Insurance.

Types of Insurance Policies for Heavy Equipment

Every construction business has diverse needs; you should tailor your insurance policies to match these. Below, Pinsonneault outlines the key coverage options you should consider:

- Inland Marine Insurance protects machinery during transport or while temporarily stored at job sites. This coverage is crucial because equipment is frequently moved between sites, increasing the risk of damage or theft during transit.

- Commercial Property Insurance: Protects equipment housed at listed locations on your policy against risks like fire or other covered natural disasters.

- General Liability Insurance is essential for third-party injury or property damage claims arising from equipment use. Construction sites are high-risk environments, and this coverage could shield businesses from financial liability if heavy equipment accidentally causes injury or damages property.

For example, a business that frequently moves heavy equipment between projects will benefit from inland marine insurance. Customizing your policy to meet your specific needs ensures maximum protection.

What Risks Does Heavy Equipment Insurance Cover?

By working with an agent, Pinsonneault emphasizes that insureds can “be matched with an insurance company offering coverage that best suits your needs and the agent has had good experiences with.”

With the right policies tailored to your business, heavy equipment insurance can offer protection options against a wide array of risks. Pinsonneault lists some of them below:

| Theft and Vandalism: Jobsites are prime targets for equipment theft. The National Equipment Register estimates theft costs construction businesses around $400 million annually in the U.S. Insurance selections can help cover replacement costs and repair damages. | Transit Accidents: Equipment damage during transportation can lead to costly delays, but insurance selections can alleviate these burdens. |

| Natural Disasters: Coverage for weather-related events like wildfires or hurricanes safeguards your machinery. (Flood is often excluded unless endorsed.) | Operational Hazards: Include incidents like rollovers or accidental damage caused during operation. |

Optional add-ons, such as replacement cost endorsements, allow you to receive compensation reflecting current market prices rather than depreciated values, providing enhanced financial stability in the event of a loss.

What Factors Influence the Cost of Heavy Equipment Insurance?

Various factors reflecting your business’s unique needs and risks influence the cost of heavy equipment insurance . The type of equipment you use is one of the most significant determinants; high-value machinery like cranes or specialized equipment tends to carry higher premiums.

- What You Can Do: When it comes to protecting this expensive equipment, Pinsonneault mentions a couple of tricks companies often use. “You can prevent losses by locking up equipment or adding GPS tracking. Companies use various methods, such as gates and fencing, to make machinery inaccessible.”

“Someone with well-maintained equipment that’s difficult to steal could pay lower rates compared to a company leaving equipment on an unsecured site.”

“I recommend registering your equipment on the National Equipment Register (NER),” Pinsonneault adds. “The NER has an online tracking system for large equipment so when something is stolen, you can send in your police report. They will send notifications to local, state, and federal law enforcement, and you’re much more likely to recover something.”

Similarly, the age and condition of your equipment play a role, with older or poorly maintained machinery being more costly to insure. The frequency of use and the nature of the projects you undertake also impact your rates, as heavy wear or high-risk environments increase the likelihood of claims.

- What You Can Do: Pinsonneault recommends maintaining a regular maintenance schedule and keeping detailed documents on upkeep and routine inspections to demonstrate to your carrier your commitment to the safety of your business and protecting your machines and workers.

Learn More: Loss Control Tips for Construction

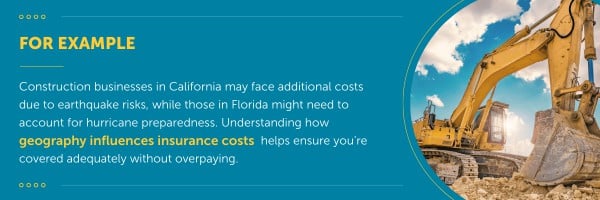

Your business’s location is another critical factor in determining insurance premiums. Regions prone to severe weather events like hurricanes or floods may see higher rates. Local regulations and state insurance requirements further shape the coverage you’ll need.

- What This Means: Pinsonneault notes that a company’s home state is a large contributing factor for insurers. “Insurers may place some consideration to the three or four states your equipment travels to. You can usually expect your rates to be based on how hazardous your home location is.”

By understanding these factors, you can effectively make informed decisions to balance cost and coverage.

Proactive Risk Management to Lower Costs

Reducing risks is essential for safety and insurance cost management. Regular machine maintenance can prevent breakdowns and extend its lifespan, making it less risky to insure; comprehensive training programs for operators can also reduce accidents, leading to fewer claims.

Securing your jobsite with measures like surveillance cameras or on-site guards minimizes the threat of theft. Partnering with an insurer offering risk assessment services can provide additional insights tailored to your operations, further lowering premiums over time.

Learn More: Central’s Construction Loss Control Specialist

What to Look for in an Insurance Carrier

Selecting the right insurance provider is as important as choosing the right coverage. Look for carriers with industry expertise, as they understand the unique challenges construction businesses face. Customizable policies ensure you’re only paying for the coverage you truly need.

Pinsonneault highlights the importance of working with an experienced agent, “Agents familiar with construction insurance can guide businesses through complex coverage needs and help find carriers with the best track record for handling claims.”

Efficient claims support is another critical factor, as it helps minimize downtime in the event of an incident. Building a relationship with a carrier that prioritizes your success makes all the difference in protecting your operations.

“We focus on meeting contractors’ unique needs with tailored coverage and specialized loss control support,” Pinsonneault explains. “Our experts understand the risks construction companies face and work to improve safety and minimize downtime.”

At Central Insurance, we understand the unique challenges faced by construction businesses. We’ve designed our specialized policies to address risks associated with heavy equipment, offering comprehensive coverage for theft, transit damage, operational hazards, and more.

Learn More: Designing the Future of Construction Underwriting at Central

If you’re ready to protect your heavy equipment with an experienced partner, contact a Central agent today to discuss your needs and get a personalized quote.

The information above is of a general nature and your policy and coverages provided may differ from the examples provided. Please read your policy in its entirety to determine your actual coverage available.

Products underwritten by Central Insurance and affiliated companies.

Copyright © 2025 Central Insurance. All rights reserved.

Comments on " How Much Does Heavy Equipment Insurance Cost?" :